Governance Warfare in Practice: African Mineral Corridors

How contract architecture, processing chokepoints, and debt structures determine who controls African mineral corridors before a single rail car moves.

Editor’s note: This is a longer piece than usual. A PDF version is available to download for your convenience.

African mineral corridors are now the most contested theater of economic and legal warfare. The competition unfolding across the Democratic Republic of Congo (DRC), Angola, Zambia, and Guinea is not primarily over resources or infrastructure. It centers on the administrative architecture through which minerals move: contract terms, concession structures, financing arrangements, regulatory frameworks, and processing access that determine who governs corridor systems and who captures value within them. These systems fix outcomes before market or military dynamics become decisive. Most current analysis does not engage the system at this level.

The analytical framework applied here – governance warfare – treats administrative systems not as background conditions but as contested terrain, and the instruments embedded within them as the primary means of strategic competition.

What follows maps that system.

The Terrain

Every mineral corridor operates across three layers. The resource layer encompasses extraction: mines, deposits, and production capacity. The transport layer governs movement: rail, port, and shipping networks. The administrative layer structures control: licensing, contracts, financing terms, concession architecture, processing access, and debt relationships.

Most analysis concentrates on the first two. The third is where competition is decided.

Two corridors make the system visible. The Lobito Corridor forms a sort of V-shape across southern-central Africa, linking the DRC and Zambian Copperbelts to Angola’s Atlantic coast. In Guinea, Simandou – the world’s largest untapped high-grade iron ore deposit – is now operational after decades of legal and commercial conflict. Each illustrates how administrative architecture is constructed, contested, and defended.

Both, however, operate within a single system constraint that must be understood first.

The Layer No One Is Watching

Control of processing allows China to dominate the system without controlling every mine or corridor.

According to the International Energy Agency (IEA), China holds the leading refining position for 19 of 20 strategic minerals, with average market share around 70 percent. In cobalt – the mineral most central to African corridor competition – the concentration is even more extreme. A 2024 USGS‑authored study in Mineral Economics found that Chinese firms control 62 percent of cobalt mine materials entering the refining pipeline, 95 percent of refined commercial-grade cobalt chemicals, 85 percent of battery-grade cobalt sulfate, and 91 percent of the cathode precursor materials used in lithium-ion battery production.

This structure allows materials to be mined outside China, by non-Chinese firms, and exported through non-Chinese corridors – yet still pass through Chinese processing facilities before reaching usable form. The refining chokepoint operates independently of control over the resource or transport layers. It is an administrative position that exerts leverage across the entire system without requiring physical presence at the point of extraction.

Beijing reinforces this position through deliberate market intervention. State-backed firms systematically overproduce to suppress global prices and drive out non-Chinese competitors. According to a CSIS analysis, between May 2022 and May 2025, cobalt prices fell 59.5 percent. The only active US cobalt mine – Jervois in Idaho – opened and closed within a single year. Nickel prices fell 73.1 percent, forcing BHP to shutter Nickel West in Australia. Lithium prices fell 86.8 percent. In each case, Chinese firms absorbed losses no commercially driven actor could sustain. This is economic warfare conducted through market structure.

The first serious attempt to challenge this position on the African continent is a cobalt sulfate refinery in Zambia, designated as an EU strategic project and targeting commissioning in 2026. Whether it can operate competitively against processing capacity optimized over three decades – while Beijing retains the ability to manipulate feedstock pricing at will – remains an open question. Its existence, however, marks the first time the processing layer has been contested where the minerals themselves are extracted.

Everything that follows in the Lobito and Simandou analysis operates within this constraint. Transport-layer competition that does not address processing dominance alters the routes minerals travel without changing who captures value or exercises leverage. A Western-backed railroad improves logistics. It does not, by itself, reconfigure the governance architecture. The system it enters is already structured.

The Lobito Corridor: Node by Node

The DRC Arm: A Captured Node Under Renegotiation

The administrative architecture of the DRC’s mining sector was not captured overnight. It was constructed over two decades through a single foundational instrument, then reinforced through acquisition, debt, and market control until it became the defining feature of the node.

The instrument was Sicomines. Signed in 2008, the Sino-Congolaise des Mines agreement gave a Chinese consortium – China Railway, Sinohydro, Zhejiang Huayou – a 68 percent stake in a copper-cobalt joint venture in exchange for infrastructure investment. The state mining company Gecamines retained 32 percent. It was called the contract of the century. The terms tell a different story. By the time the DRC’s own transparency body examined the deal, Chinese companies had earned nearly $10 billion in profits. The DRC had received $822 million in infrastructure. AidData found Sicomines had contracted $7.61 billion in debt between 2008 and 2020 – more than double the original agreement. The first Chinese export-import bank loan carries a 6.1 percent fixed rate over 25 years; the second carries a floating rate plus 3 percent over another 25 years. Sicomines remains exempt from taxes until 2040.

That is not a joint venture. It is an administrative position embedded in contract architecture and reinforced by debt.

The position deepened. In 2016, CMOC acquired Tenke Fungurume – once the crown jewel of US mining in the DRC under Freeport-McMoRan – for $2.65 billion, financed by six Chinese state banks. A Freeport legal executive warned an Obama administration national security adviser, General James Jones, about the imminent sale but was told, “There’s no one that’s going to be interested in that.” By 2025, Chinese firms owned or held stakes in 15 of the largest copper and cobalt mines in the country. They controlled roughly 80 percent of total mining output.

Kinshasa has begun to fight back, and the tools it is using are themselves economic and legal warfare instruments.

In February 2025, the DRC halted all cobalt exports. Prices had hit a nine-year low, driven by deliberate overproduction from Chinese-controlled mines – the same pricing dynamic now operating at the resource node itself. The ban held for eight months. Cobalt prices rallied 170 percent from their January lows. Chinese imports of cobalt intermediates fell 72 percent year-over-year by July. Glencore and CMOC declared force majeure.

But the ban also imposed significant fiscal costs on Kinshasa, with officials acknowledging lost tax and royalty revenue and rising budget pressures as cobalt exports remained suspended. Chinese processors had built significant inventory buffers before and during the ban, allowing them to maintain exports and production even as imports of cobalt intermediates fell sharply. Material continued to flow through bonded zones and long-term contracts. The sovereign had leverage. Exercising it was costly, and the structural position it was pushing against had been designed to absorb exactly this kind of pressure.

In October, Kinshasa shifted to a quota system. Annual exports capped at 96,600 tonnes for 2026 and 2027 – less than half of 2024 output – and placed under the exclusive management of ARECOMS, a new state regulator with sole authority to issue, allocate, and revoke export permissions. Ten percent of volumes were reserved for strategic national projects. The measure centralizes administrative control over the country’s most strategic export – a governance warfare counter-move conducted through regulatory architecture that reverses, rather than extends, deregulation and liberalization

The renegotiation of Sicomines followed. A fifth amendment in March 2024 committed $5.5 billion in additional infrastructure spending through 2040, conditional on copper prices. Gecamines gained marketing rights over 32 percent of production. In March 2026, a comprehensive audit was launched covering the entire 2008-2024 period – the first time the full financial and operational architecture of the deal has been subjected to independent examination. The EITI transparency findings that revealed the $10 billion-to-$822 million imbalance were the catalyst. Transparency functioned as an economic warfare instrument: public information that shifted the leverage balance at a captured node.

Then the United States entered the administrative layer.

The US-DRC Strategic Partnership Agreement, signed December 4, 2025, creates a Strategic Asset Reserve (SAR) – a designated pool of critical mineral assets and unlicensed exploration areas where US companies receive preferential access and exclusive three-year negotiation windows. A Joint Steering Committee oversees allocation. The DRC commits to regulatory reform. A security memorandum of understanding is under development. The first tangible result arrived in January 2026: 100,000 tons of copper from Tenke Fungurume shipped to the United States when Gecamines exercised its marketing rights independently of Chinese intermediaries for the first time.

This is administrative terrain seizure. The SAR restructures who has access to the next generation of mineral assets. The regulatory reform provisions reshape the environment in which future contracts will be negotiated. The security linkage ties mineral access to the US role in mediating the DRC-Rwanda conflict – a dependency relationship that mirrors, in structure if not in scale, the infrastructure-for-minerals model it is designed to displace.

The agreement was not presented to the Congolese parliament. Congolese lawyers filed a constitutional challenge in January 2026. Civil society organizations have called it a “sovereignty erosion” dressed as partnership. The M23 rebel alliance called it unconstitutional. The parallels to Chinese engagement are structural. Both architectures use administrative instruments to embed preferential access, both bypass legislative oversight, and both tie mineral governance to broader strategic relationships that constrain the sovereign’s option space.

The difference is not in method, but in timing. China’s administrative architecture at this node is two decades deep, while the American architecture is months old.

The Angola Vertex: A Chinese-Built Chokepoint Under Western Concession

The Lobito Corridor’s physical infrastructure was built by China. Its administrative concession is held by a Western consortium. Its governance is constrained by debt. Angola is the chokepoint – and it is compromised in every direction.

The Benguela Railway was rebuilt entirely by China between 2006 and 2014 under a $2 billion rail-for-oil program. Chinese engineers restored 67 stations, bridges, and rolling stock. The design capacity was 20 million tons of cargo and four million passengers annually. In 2023, a consortium of Trafigura, Mota-Engil, and Vecturis secured a 30-year concession to operate the railway and mineral terminal. In December 2025, the consortium closed a $753 million financing package – $553 million from the US Development Finance Corporation (DFC) and $200 million from the Development Bank of Southern Africa. The United States and Europe did not build this corridor. They are offering management models, logistics optimization, and governance frameworks after losing the construction race a decade ago.

The “Western” consortium is not fully Western. Mota-Engil, one of LAR’s three principal companies, is 32.4 percent owned by China Communications Construction Company, a Chinese state-owned enterprise. Chinese state capital is embedded inside the operating entity the DFC is financing. The transport layer is formally under Western concession. The ownership layer is partially Chinese. The physical infrastructure was entirely Chinese-built.

Angola itself operates under severe governance constraints. Angola has borrowed over $46 billion from China since 2000, though outstanding debt now stands at under $8 billion after recent repayments. President Lourenço promised reform but further centralized power and preserved the extractive economic order. The government’s institutional reform program has fallen short, with corruption and patronage networks proving resistant. Oil production is declining. Elections will be held again in August 2027. Lourenço has shifted foreign policy toward Washington and positioned the corridor as his diplomatic centerpiece, but the institutional depth to govern the chokepoint independently has not been established.

The corridor is attracting more than commercial interest. In August 2025, Angolan intelligence arrested two Russian nationals linked to Africa Corps – formerly Wagner Group – for alleged disinformation operations and intelligence collection on the Lobito Corridor ahead of the 2027 election.

Angola is not treating the Lobito Corridor as a one-off. In December 2025, the Ministry of Transport launched an international tender for the Namibe Corridor: an 855-kilometer railway and port system in southern Angola, with a 30-year concession extendable to 50 years, including future rail connections to Namibia and Zambia. The Moçâmedes-Menongue line traverses one of Southern Africa’s most mineral-rich regions. Bids are due May 4, 2026. This is not an isolated project. It is a pattern: Angola systematically concessioning its transport infrastructure to position itself as a multi-corridor logistics hub; a governance model for the vertex.

Under Biden, the Lobito Corridor was framed as a climate-transition project. Under Trump, it has been reimagined as a geoeconomic instrument, designed to dilute Chinese dominance and strengthen US leverage over critical materials. The framing shifted. The structural constraints at the vertex did not.

The Zambia Junction: Strong Institutions At A Structurally Constrained Node

Zambia is one of the key nodes where westbound Lobito infrastructure intersects with existing eastbound export routes. The Lobito Corridor runs west through Angola to the Atlantic under a Western-backed concession financed by the DFC. The TAZARA railway runs east through Tanzania to Dar es Salaam and the Indian Ocean under a Chinese 30-year concession – a $1.4 billion revitalization by China Civil Engineering Construction Corporation, the original builder. The groundbreaking took place in Lusaka on November 20, 2025, attended by Zambian President Hakainde Hichilema, Chinese Premier Li Qiang, and Tanzanian Vice President Emmanuel John Nchimbi.

Zambia’s institutional environment is the strongest in the corridor. Peaceful transfers of power. Democratic governance. Copper output targeting one million tons in 2026. Major expansions underway from First Quantum, Barrick, Sinomine, and KoBold Metals. A cobalt sulfate refinery – Africa’s first – targeting commissioning in 2026 and designated as an EU strategic project. This is the node with the strongest domestic institutions and the most active attempt to break the processing-layer constraint.

But institutional strength at one node does not determine corridor-level outcomes when administrative terms are set elsewhere.

TAZARA is more than a railway rehabilitation. China, Tanzania, and Zambia issued a joint statement on building a “TAZARA Railway Prosperity Belt” – committing to special economic zones, industrial parks along the line, trade integration, zero-tariff measures for African countries maintaining Chinese diplomatic relations, and capacity building. China is “ready to work with Zambia” to step up cooperation in judicial, police, law-enforcement and other areas. This is administrative terrain construction embedded in an infrastructure concession from inception: economic integration, institutional alignment, and security cooperation packaged as development partnership.

The junction dynamic is straightforward. Whichever corridor captures the dominant share of Copperbelt mineral throughput shapes the governance terms for the region. Tanzania’s finance ministry projects TAZARA will eventually transport 3 million metric tons of minerals annually. The Lobito Corridor targets comparable volumes but its DRC segment operates at less than 5 percent of capacity. Until the Western-backed corridor is fully functional across all three countries, the administrative architecture attached to the Chinese-backed eastern route has a structural throughput advantage.

Zambia’s strong institutions give it the capacity to negotiate corridor terms. They do not give it the capacity to determine which corridor the minerals flow through. That decision is being made at the infrastructure layer, and the eastern route is further along. Taken together, the DRC arm, the Angola vertex, and the Zambia junction show how administrative architecture can be captured at the node, compromised at the vertex, and contested at the junction – and how long it takes to shift that structure once it is in place.

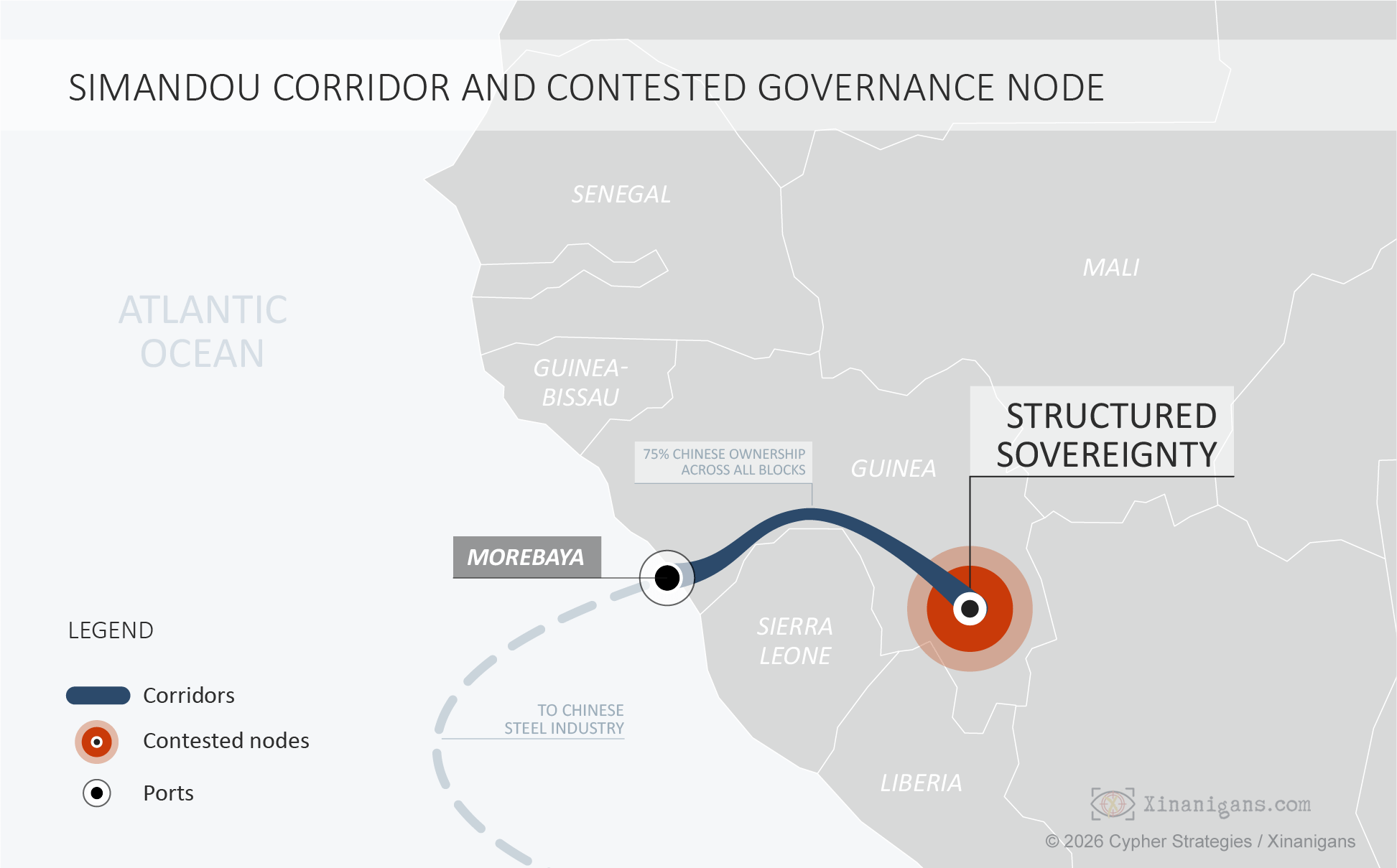

Simandou: Structured Sovereignty Under Test

Simandou tests whether formal sovereignty can withstand administrative dominance when the operating architecture runs through a competitor’s networks.

The Lobito Corridor demonstrates how administrative control over corridor terrain is built, contested, and re-entered over time. Simandou presents a different question. Guinea embedded sovereignty provisions into the concession architecture before the first ore shipped. The formal tools exist; the question is whether they hold when the operating architecture runs through a competitor’s networks.

Simandou is the world’s largest untapped high-grade iron ore deposit: 65 percent iron content, suitable for lower-emissions green steel production. Operations began in November 2025. The first commercial shipment of 200,000 tonnes arrived in eastern China in January 2026. At full build-out, production targets approximately 120 million tonnes per year – enough to materially reshape global seaborne iron ore supply and trade flows, predominantly into China.

The ownership architecture is straightforward. Winning Consortium Simandou (WCS) controls Blocks 1 and 2 – a Singapore-Chinese partnership dominated by Chinese interests including China Baowu Steel Group, the world’s largest steelmaker. Blocks 3 and 4 are held by Rio Tinto at 53 percent in joint venture with Chinese state-owned enterprises led by Chinalco at 47 percent. Even the nominally Western side is nearly half Chinese-owned. Across the full project, Chinese interests represent approximately 75 percent of ownership concentration.

Guinea’s governance tools are more structured than anything in the Lobito system. The state holds 15 percent free carry equity in all blocks, plus the same stake in the railway and port, with veto rights over strategic decisions. The concession runs 35 years for the integrated mine-rail-port system. Completed infrastructure becomes Guinean state property, creating permanent national assets beyond the mine’s operational lifespan. The shared infrastructure entity – Compagnie du TransGuinéen, co-owned by both consortia at 42.5 percent each and the state at 15 percent – operates more than 600 kilometers of new railway and a deep-water port. Guinea has announced its first sovereign wealth fund, the Fonds de Richesse Simandou, capitalized at approximately $1 billion and expected to launch in 2026.

On paper, this is a different model from the DRC. Guinea negotiated equity, veto authority, infrastructure reversion, and a sovereign wealth mechanism before production began. The formal architecture is designed to prevent the kind of structural capture that Sicomines represents.

The stress test is whether those tools function when the operating reality runs in a single direction through a competitor’s commercial networks. The firms mining the ore are Chinese or Chinese-partnered. The firm buying the ore is overwhelmingly the Chinese steel industry. The technical and operational knowledge resides in the consortium, not the state. Revenue projections depend on Chinese demand. The 15 percent equity stake and the veto right are governance instruments, but they operate inside a commercial architecture where 75 percent of the decisions, the capital, the expertise, and the market destination are Chinese.

A veto right that cannot be exercised without jeopardizing the revenue stream exists as formal power, not functional power.

The history reinforces the question. Simandou’s administrative terrain has been contested through legal, political, and commercial warfare for two decades. Rio Tinto was stripped of the northern blocks in 2008 when a dying president awarded them to Beny Steinmetz’s BSGR. Steinmetz lost his final appeal on bribery charges in Swiss courts in March 2025. A subsequent president annulled the BSGR rights on corruption grounds, triggering years of additional litigation. BSGR relinquished claims in a 2019 settlement. The current structure emerged from this wreckage – not from strategic design by a stable government, but from the accretion of deals, revocations, lawsuits, coups, and settlements over twenty years.

Guinea is now governed by a military junta under Colonel Mamady Doumbouya, who took power in 2021. The government published two sets of Simandou project agreements at the end of 2025, a transparency commitment. Guinea also signed a critical minerals MoU with the United States at the February 2026 ministerial in Washington, a signal that Conakry may be positioning for the same kind of competitive dynamic visible in the DRC. But a military government building sovereignty instruments over the world’s largest iron ore project introduces a question the formal architecture cannot answer: institutional durability. Equity stakes survive changes in government. Governance capacity may not.

Simandou is deliberately structured not to replicate the DRC’s experience. The capture is less deep, the tools are more developed, and the concession architecture was designed with sovereignty in mind. Yet the operating reality still flows through Chinese commercial networks at every layer: ownership, expertise, infrastructure construction, market destination. Whether formal governance tools can hold against that current, over a 35-year concession, under a government whose own legitimacy is contested, is the test of structured sovereignty that Simandou poses to the entire system.

The Escape Valve

Everything described above assumes sustained external commitment to African corridor investment. That assumption is fragile.

In October 2025, President Trump and President Xi reached an agreement to stabilize trade relations after months of escalating mineral warfare. China issued general licenses for rare earths, gallium, germanium, antimony, and graphite for US end users. The US extended tariff exclusions.

Washington secured mineral access through bilateral accommodation with Beijing, not through African diversification.

This dynamic reduces the strategic necessity of African corridor competition. The Lobito financing, the DRC Strategic Partnership, the Zambian processing investments, and the Simandou MoU all assume sustained US commitment to building alternative supply chains through Africa. The escape valve makes that assumption unreliable. If Washington can negotiate directly with Beijing when pressure intensifies, African partnerships become secondary options: useful for long-term positioning but not urgent enough to sustain the political capital, institutional attention, and financial commitment required to compete at the administrative layer. Each resort to bilateral accommodation further entrenches Chinese processing dominance while weakening incentives for Western capital to invest in alternative processing nodes.

African governments are already reading the signal. When the US-China tariff détente included mineral provisions, it demonstrated that the two largest economies will prioritize bilateral accommodation over competition in the Global South. This introduces instability into every corridor investment premised on great-power competition as the driver. The infrastructure may be built. The administrative commitment behind it may not endure.

What Practitioners Are Missing

The prevailing analytical frame for African mineral competition focuses on assets, infrastructure, and security arrangements. What it does not map is the administrative architecture that determines outcomes before those instruments are relevant: contract terms, processing chokepoints, pricing mechanisms, debt structures, concession design, and regulatory frameworks. These same instruments also structure environmental and community impacts along the corridors, determining where costs are concentrated and who has standing to contest them.

The current assumption is that control is visible. Who owns the mine. Who built the railroad. Who signed the partnership. The reality across the Lobito Corridor and Simandou is that control is embedded. In tax exemptions extending to 2040. In processing monopolies operating off-continent. In debt relationships constraining sovereign decision-making. In Chinese state capital inside nominally Western consortia. In formal governance tools that cannot be exercised without jeopardizing the revenue they were designed to capture.

The dominant approach is to compete at the transport layer – build corridors, finance rail, secure port access. The constraint is that outcomes are determined at the resource and processing layers. The DRC’s administrative architecture was captured through contracts and debt over two decades. Angola’s chokepoint is formally controlled but structurally compromised. Zambia’s strong institutions cannot determine which corridor captures throughput. Guinea’s sovereignty provisions face a 35-year stress test against an operating reality that flows in a single direction. And the processing chokepoint operates independently of all of them – off-continent, optimized over three decades, reinforced by deliberate market manipulation.

A new railroad is a more efficient way to export on someone else’s terms if the contract architecture and processing access haven’t changed. Any corridor strategy that does not include binding commitments on processing and contract architecture will, on its own terms, reproduce this dynamic rather than displace it.